In 2024, the municipal bond market saw significant outflows, marking tax-deadline selling pressure. LSEG Lipper reported a total of $1.47 billion in outflows from municipal bond mutual funds. These outflows were largely driven by higher rates and tax liabilities, resulting in negative flows from both exchange-traded funds and open-end funds. Notably, high-yield funds experienced their first outflows since January 3, with a negative $48 million in flows. This trend highlights the impact of market volatility and changing interest rates on investor behavior within the municipal bond market.

Municipal Bond Pricing and Yield Ratios

Despite the outflows, the municipal bond market remained relatively stable, with new issues pricing throughout the week. U.S. Treasury yields rose during this period, impacting the overall market sentiment. The muni-to-Treasury ratio varied across different maturity periods, reflecting the changing dynamics within the bond market. Traders observed a curve bifurcation in bond maturities, with significant interest in maturities ranging from 2037 to 2040. This trend suggests a shift in investor preferences based on yield and maturity characteristics.

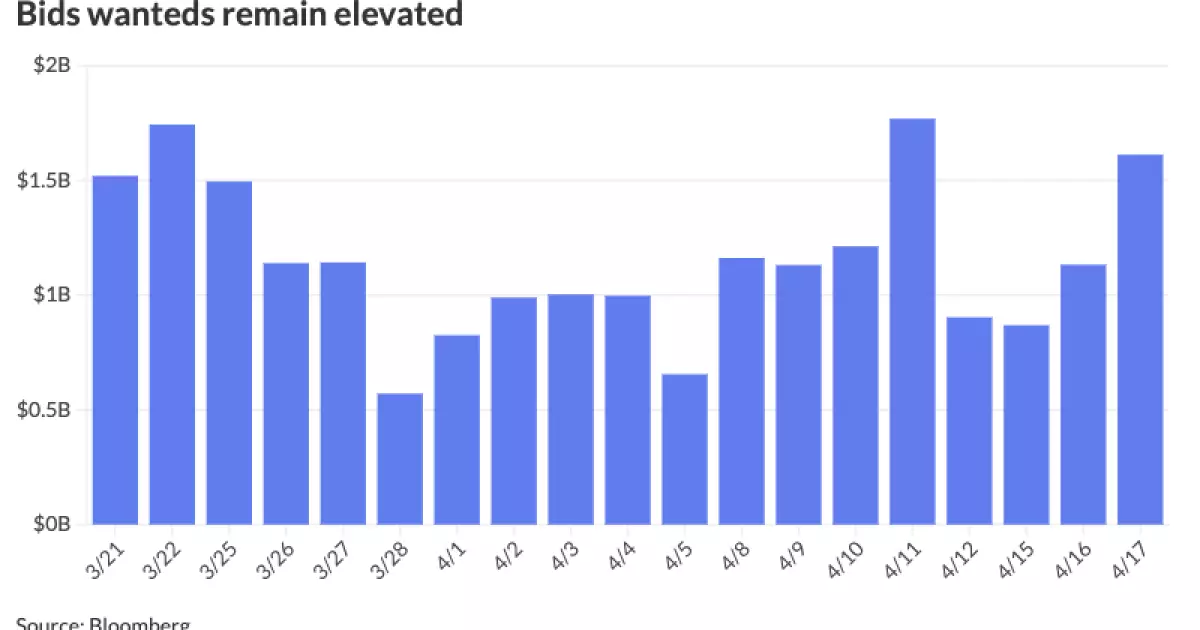

Tax-exempt trade flows in the municipal bond market indicated a divergence in trading patterns, with a mix of short-term and long-term maturities attracting attention. The movement of taxable yields also influenced the direction of municipal bond prices, creating a more defensive trading environment. Despite challenges in reinvestment flows and elevated supply levels, the market continued to function efficiently, aided by healthy levels of new issuance. Price discovery remained strong, supported by the overall level of new municipal bond issuance.

Market participants noted a balance between supply and demand, with a consistent flow of new issuances entering the market. Dealer inventories declined, signaling a shift in trading patterns towards customer orders. Despite increased rate volatility, munis displayed resilience, with new inquiries benefiting from retraced yields. The overall demand for municipal bonds remained high, driven by attractive income levels. Investors found tax-exempt deals with yields around 4% appealing in the current fixed-income landscape.

Municipal CUSIP request volume increased in March, reflecting a year-over-year growth in identifier requests for new municipal securities. Texas led state-level municipal request volume, followed by New York and Wisconsin. The availability of new CUSIPs indicates continued activity in the municipal bond market, with ongoing interest from investors and issuers alike.

Yield curves across different indices exhibited variations in response to changing market conditions. While the municipal bond market experienced stability, Treasuries showed firmer yields across the curve. This divergence in yield movements highlights the complexity of the current market environment and the need for investors to carefully monitor both municipal and Treasury bond dynamics.

Overall, the analysis of municipal bond market outflows in 2024 reveals a nuanced picture of investor behavior, market trends, and supply-demand dynamics. Despite challenges such as tax liabilities and higher rates, the municipal bond market continues to attract investor interest, driven by attractive income levels and healthy levels of new issuance. As the year progresses, monitoring market conditions and staying informed about changing trends will be essential for investors seeking opportunities in the municipal bond market.