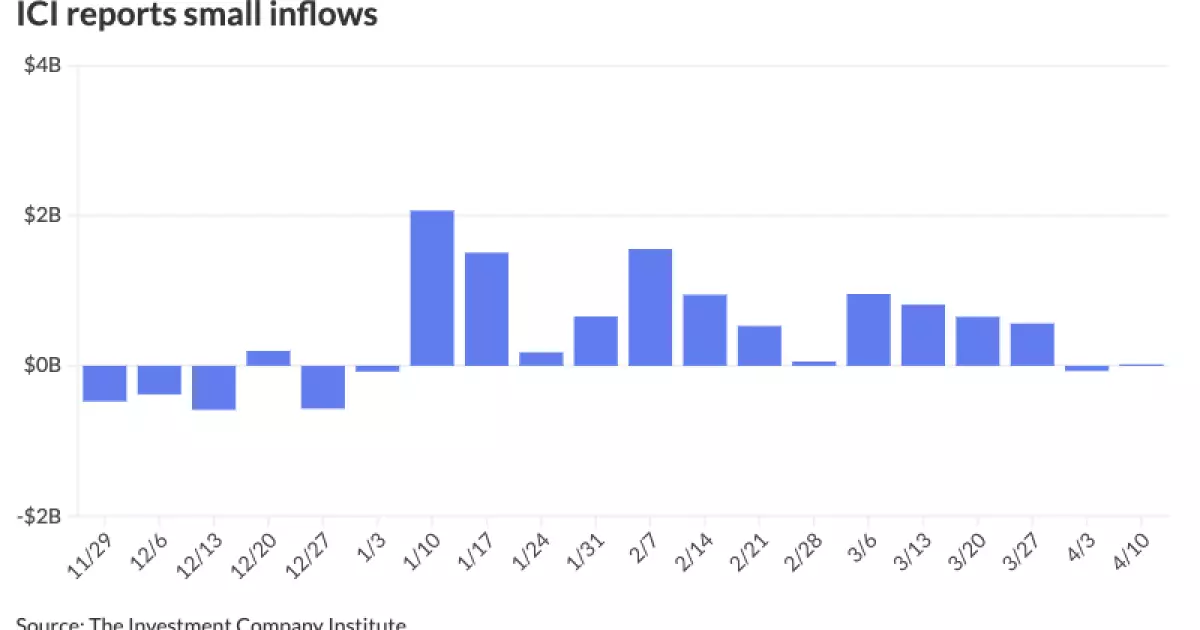

The municipal bond market experienced minimal fluctuations on Wednesday due to a slowdown in supply and minor inflows into muni mutual funds. Despite U.S. Treasury yields decreasing and equity markets displaying losses, the sector remained relatively stable. Investment Company Institute data revealed that investors contributed $18 million to municipal bond mutual funds in the week ending April 10, following a previous week of $69 million in outflows. Additionally, exchange-traded funds witnessed inflows of $944 million during the same period.

J.P. Morgan strategists indicated that muni AAA HG curve yields reached new year-to-date highs, with the overall muni HG curve demonstrating superior performance compared to the broader fixed income market in recent times. Despite the “rapid” UST volatility affecting muni yield movements, Jeff Timlin from Sage Advisory noted that the new-issue market continued to exhibit strength. The absolute yields in the market remain attractive, especially considering the trading range over the past three years and the projections for lower rates in the year ahead.

The article highlighted that two-year investment-grade muni ratios compared favorably to taxable fixed-income, but as the curve extended to the five- to 10-year range, tax-exempt investments became more attractive. This was particularly evident in the 10-year spot, where taxable options outperformed tax-exempts. Refinitiv Municipal Market Data data indicated various ratios across maturities, with tax-exempt 30-year AA munis appearing to offer value when considering taxable equivalent yields.

Looking ahead, market analysts anticipated a softer period in April due to an increase in expected supply until early June, which may impact market performance heading into the summer months. Timlin suggested that this temporary softness could present an opportunity for investors to reallocate capital, especially with reinvestment dollars set to pick up from June through August. The market conditions indicated by ICE Data Services and other sources suggested a potential underperformance in the less favorable technical environment expected in April.

Several significant bond issuances were scheduled for pricing on Thursday, including offerings from the Arizona Board of Regents, Washington State Housing Finance Commission, Oklahoma Capital Improvement Authority, Oregon Department of Administrative Services, and Wake County, North Carolina. Additionally, competitive sales from Albuquerque, New Mexico, and Clark County School District, Nevada, were set to take place, indicating continued activity in the municipal bond market.

The municipal bond market demonstrated resilience in the face of market volatility and external factors impacting yields and supply dynamics. Despite ongoing fluctuations, investors remained optimistic about the long-term prospects of tax-exempt investments and the relative value they provide in comparison to taxable fixed-income options. With upcoming primary offerings and a period of expected market softness, investors are advised to monitor the situation closely and consider potential opportunities for deploying capital effectively in the municipal bond sector.