The municipal market continues to face challenges as investors navigate through a landscape of large deals in the primary market and improving U.S. Treasuries. The focus on the primary market has overshadowed the secondary market as investors grapple with the influx of new issuances and the implications for muni yields. This article critically analyzes the current conditions of the municipal market and provides insights into the challenges and opportunities that lie ahead.

The increase in issuance this week has created an “ample opportunity” for investors to buy paper, but it has also kept muni yields at an elevated level. The large new-issue deals are expected to be well-received as institutional money managers seek large block sizes to retool portfolios. However, the bid strength from separately managed accounts and retail investors has created a bifurcated demand, with the back end of the curve not being well-supported. This imbalance poses challenges for investors seeking to find optimism in the near term.

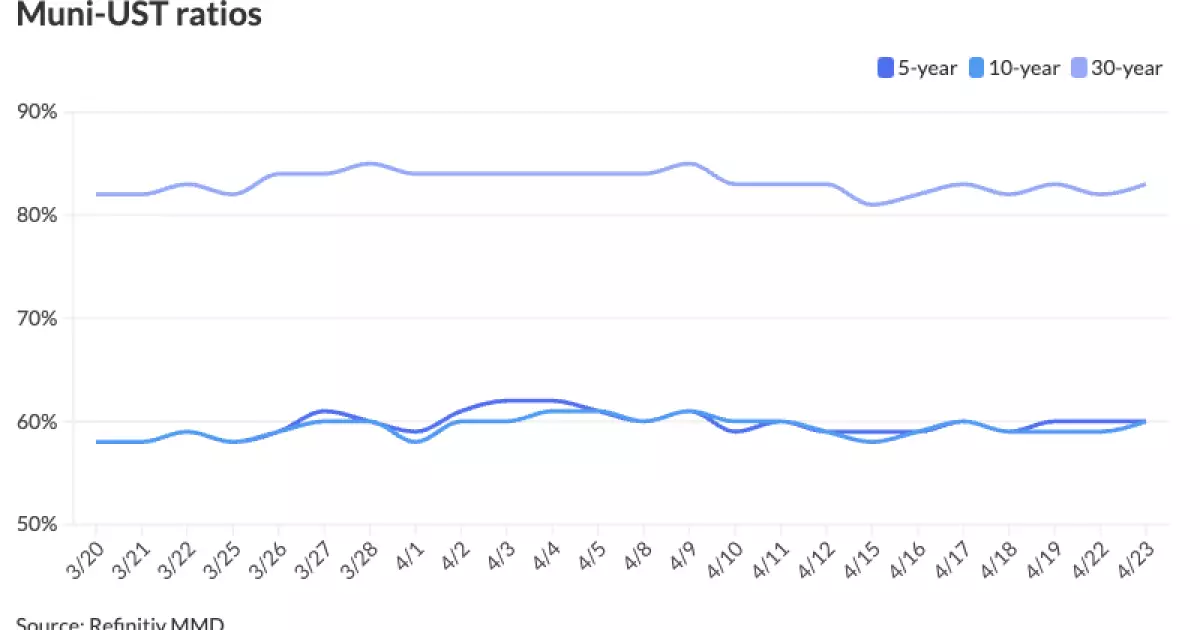

Front-end yields have held up well since the start of March, while term spreads have widened. The muni-to-Treasury ratios remain on the rich side, reflecting the new normal in the market. The strength of separately managed accounts has led to improving bond insurance penetration, highlighting the importance of nominal ratings for primary market buyers.

Investors can expect to find quality 5s on the long end with attractive yields. However, cheaper credit 4% coupons around the 20-year area may present challenges for retail buyers. As May approaches, which is known as the worst reinvestment month of the year, near-term optimism becomes harder to find. Despite these challenges, well-structured credits in the primary market are likely to see strong demand, providing opportunities for income-biased buyers.

The competitive market landscape features a range of upcoming deals, including the $2 billion Brightline Florida Passenger Rail Project bonds and the $370.32 million RWJ Barnabas Health Obligated Group bonds. These deals, along with others set to be priced in the coming days, will test investor appetite and market conditions. The market is expected to provide solid opportunities for income-biased buyers, especially those looking beyond typical retail buying ranges.

The current municipal market situation is characterized by a focus on the primary market, elevated muni yields, and a bifurcated demand from institutional and retail investors. The challenges posed by the influx of new issuances and the imbalance in demand require careful navigation by investors. However, the market also presents opportunities for income-biased buyers to capitalize on well-structured credits and attractive yields. As investors look ahead to the summer buying season, they must stay vigilant and adapt to the evolving market conditions to make informed investment decisions.